Top Recruitment Agencies in Saudi Arabia (KSA)

In the dynamic business landscape of Saudi Arabia — driven by Vision 2030, rapid digital transformation, giga-projects like NEOM, and expanding private sector growth — attracting the right talent has become more critical than ever. [...]

Most Read

In the Early 2000s, General Electric, an American Multinational conglomerate, experienced a crunching profit decline and stagnant stock prices. The company had to devise a performance review process that evaluated […]

Absenteeism is a crucial aspect of every workspace and impacts company culture. Some absences are avoidable, such as illness and emergencies. However, frequent absences can affect a company’s productivity and […]

Since its release in 2022, ChatGPT has quickly become one of the most widely used AI chatbot tools worldwide. One month after its launch, it set a new record by […]

It seems like every day, there’s a new development in the world of artificial intelligence (AI). But unlike many other trends, the buzz around AI is likely justified. This is […]

Attracting the best talents in the UAE has become a rat race as many companies’ HR seek to outsmart each other. Every firm is constantly strategising to attract the most […]

So much has changed over the past few years. The whirlwind of artificial intelligence (AI) advancements has transformed different human resources operations and performance management is no exception. Integration of […]

Every company wants to secure the best talent to drive its operations and innovations forward, especially in today’s competitive business environment. In the UAE, this quest for top talent is […]

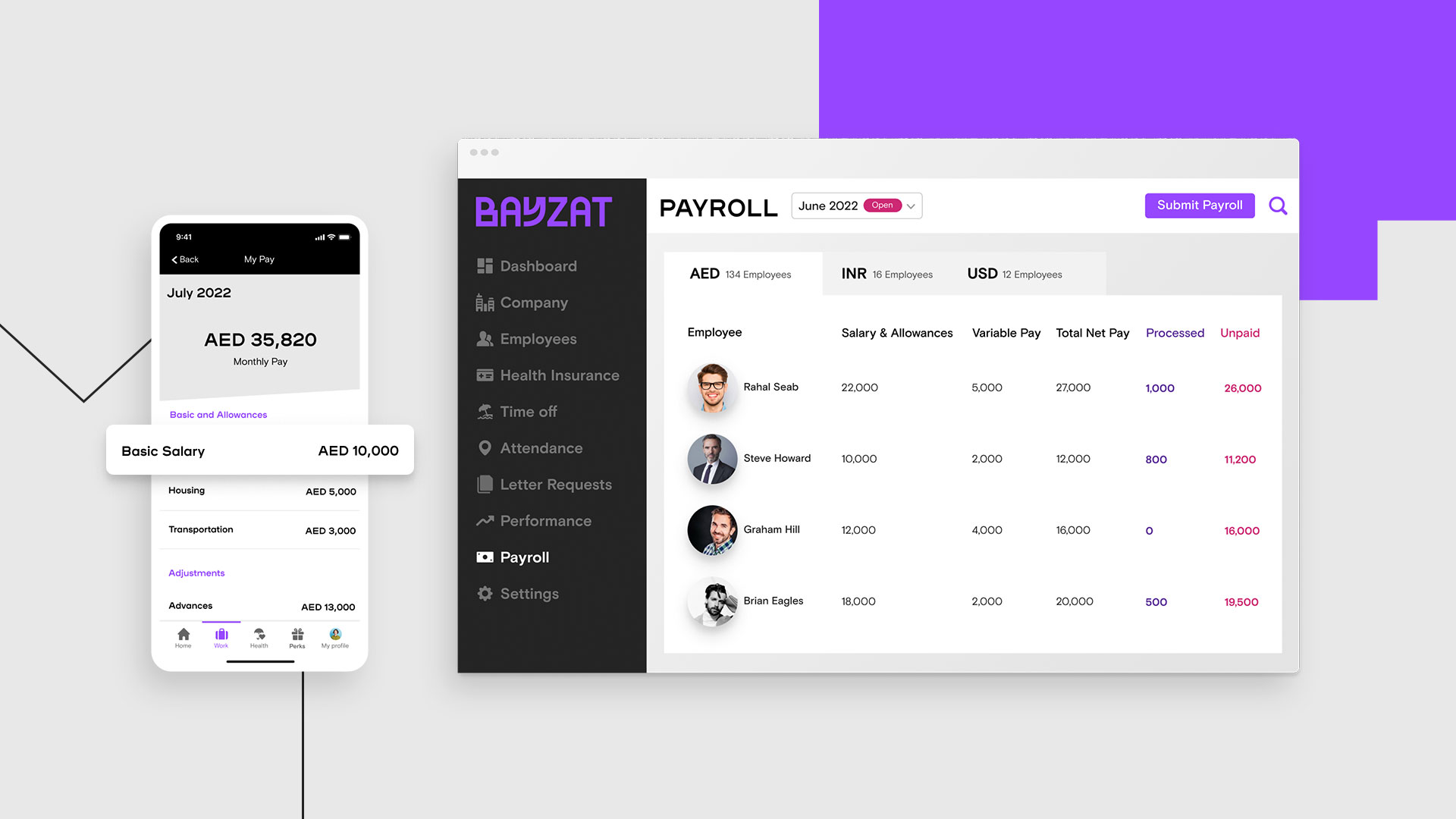

Payroll management can take a lot of time. You need to process the hours, special time-off, work-related expenses and many more for various workers, from part-time to full-time. In the […]

Employee engagement has exploded in recent years in terms of importance. But the word isn’t a meaningless buzzword. With the correct type of employee engagement, you could achieve higher productivity, […]

A coaching culture is vital for businesses in the UAE looking to increase retention. The region is notorious for having low retention rates, but a comprehensive coaching culture could change […]

Every manager and CEO knows that people make businesses succeed or fail. But managing employee performance is still too often an afterthought. In reality, if you want to make the […]

People are your most powerful asset. Employees that are happy and content at work can perform better. As your workforce becomes more productive, your business will benefit. But how can […]

HR management involves a lot of tasks, from finding new talent to ensuring current employees are looked after. It’s a lot of paperwork and communication with different players within an […]

In the dynamic business landscape of Saudi Arabia — driven by Vision 2030, rapid digital transformation, giga-projects like NEOM, and expanding private sector growth — attracting the right talent has […]

Beyond being a mere administrative formality, the employee onboarding experience can be a bit of a whirlwind with so many changes and things to remember. While there are many […]

Choosing the right HR software has become a critical decision for businesses in Saudi Arabia and the Middle East. As companies scale, expand across locations, and navigate local labor regulations, […]

In the hiring process, HR professionals often juggle more than just resumes; they manage candidate experience, consistently improve new hire quality, and much more. In this guide, we will introduce […]

Need an efficient way to handle employee onboarding process? Our onboarding and offboarding checklist offers clear steps for smooth integration of new hires and professional exits. Discover best practices in […]

Accounts Payable is the process of tracking, managing, and paying vendor invoices. Every business, big or small, has to deal with Accounts Payable (AP) but if done manually, AP can […]

Understanding HR policies in UAE is crucial for legal compliance and efficient operations. This guide provides insights into essential HR policies in UAE on recruitment, compensation, performance management, and legal […]

A multi-generational workforce has merits and demerits. Knowing how to engage such dynamism can push your organization to unprecedented growth levels, while the opposite could lead to a total collapse. […]

One common challenge UAE start-ups face is scaling their culture and imprinting the idea into talents to achieve overall goals. A company’s culture is like its DNA, defining how it […]

Attracting the best talent and holding onto the existing top performers means the company will need to have an attractive compensation package within its staff retention and hiring plan. Sometimes […]

-

In the Early 2000s, General Electric, an American Multinational conglomerate, experienced a crunching profit decline and stagnant stock prices. The company had to devise a performance review process that evaluated […]

-

Absenteeism is a crucial aspect of every workspace and impacts company culture. Some absences are avoidable, such as illness and emergencies. However, frequent absences can affect a company’s productivity and […]

-

Since its release in 2022, ChatGPT has quickly become one of the most widely used AI chatbot tools worldwide. One month after its launch, it set a new record by […]

-

It seems like every day, there’s a new development in the world of artificial intelligence (AI). But unlike many other trends, the buzz around AI is likely justified. This is […]

-

Attracting the best talents in the UAE has become a rat race as many companies’ HR seek to outsmart each other. Every firm is constantly strategising to attract the most […]

-

So much has changed over the past few years. The whirlwind of artificial intelligence (AI) advancements has transformed different human resources operations and performance management is no exception. Integration of […]

-

Every company wants to secure the best talent to drive its operations and innovations forward, especially in today’s competitive business environment. In the UAE, this quest for top talent is […]

-

Payroll management can take a lot of time. You need to process the hours, special time-off, work-related expenses and many more for various workers, from part-time to full-time. In the […]

-

Employee engagement has exploded in recent years in terms of importance. But the word isn’t a meaningless buzzword. With the correct type of employee engagement, you could achieve higher productivity, […]

-

A coaching culture is vital for businesses in the UAE looking to increase retention. The region is notorious for having low retention rates, but a comprehensive coaching culture could change […]

-

Every manager and CEO knows that people make businesses succeed or fail. But managing employee performance is still too often an afterthought. In reality, if you want to make the […]

-

People are your most powerful asset. Employees that are happy and content at work can perform better. As your workforce becomes more productive, your business will benefit. But how can […]

-

HR management involves a lot of tasks, from finding new talent to ensuring current employees are looked after. It’s a lot of paperwork and communication with different players within an […]

In the dynamic business landscape of Saudi Arabia — driven by Vision 2030, rapid digital transformation, giga-projects like NEOM, and expanding private sector growth — attracting the right talent has […]

Beyond being a mere administrative formality, the employee onboarding experience can be a bit of a whirlwind with so many changes and things to remember. While there are many […]

Choosing the right HR software has become a critical decision for businesses in Saudi Arabia and the Middle East. As companies scale, expand across locations, and navigate local labor regulations, […]

In the hiring process, HR professionals often juggle more than just resumes; they manage candidate experience, consistently improve new hire quality, and much more. In this guide, we will introduce […]

-

Need an efficient way to handle employee onboarding process? Our onboarding and offboarding checklist offers clear steps for smooth integration of new hires and professional exits. Discover best practices in […]

-

Accounts Payable is the process of tracking, managing, and paying vendor invoices. Every business, big or small, has to deal with Accounts Payable (AP) but if done manually, AP can […]

-

Understanding HR policies in UAE is crucial for legal compliance and efficient operations. This guide provides insights into essential HR policies in UAE on recruitment, compensation, performance management, and legal […]

-

A multi-generational workforce has merits and demerits. Knowing how to engage such dynamism can push your organization to unprecedented growth levels, while the opposite could lead to a total collapse. […]

-

One common challenge UAE start-ups face is scaling their culture and imprinting the idea into talents to achieve overall goals. A company’s culture is like its DNA, defining how it […]

-

Attracting the best talent and holding onto the existing top performers means the company will need to have an attractive compensation package within its staff retention and hiring plan. Sometimes […]

Get Social